.svg)

Biochar

Your board keeps hearing about "biochar" from peers and the tech press. Finance is pushing back on the price. Legal is nervous about greenwashing under CSRD and the German courts. Meanwhile, Microsoft just locked in 1.24 million tonnes over ten years, and Google signed for 100,000 tonnes through 2030—so clearly something real is happening.

Here's what you need to know: biochar isn't some experimental technology. It's already delivering over 90% of durable carbon removal tracked globally, with 3 million tonnes contracted and prices around €125–€145 per tonne. But not all biochar credits are equal. Feedstock quality, production standards, permanence testing, and verification protocols separate century-scale carbon storage from potential compliance headaches.

This guide gives you a practical, defensible buying playbook—from understanding what biochar actually is and how it's made, to evaluating projects with the same rigour your auditors will demand. You'll learn how to go from curiosity to an auditable procurement policy that can stand up to internal audit, investor questions, and regulators. No hype, no jargon—just the clarity you need to make smart decisions about one of the most scalable removal pathways available today.

Key Takeaways

- Biochar is already the workhorse of durable carbon removal, delivering over 90% of tracked durable CDR and more than 3 Mt of contracted volume, so it deserves a dedicated lane in your net-zero strategy—not a side note.

- Quality varies massively between biochar projects: feedstock choice, production process, H/Corg testing, methodology and MRV determine whether you're buying century-scale removals or taking on greenwashing risk.

- High-integrity biochar carbon credits can be aligned with CSRD, SBTi and ICVCM's Core Carbon Principles, but only if you demand robust documentation, registry records and independent ratings for each project.

- Biochar credits are more expensive than avoidance credits (typically ~€125–€145/t in 2025), but provide far higher climate confidence and durability, making them a strong candidate for hard‐to‐abate residual emissions in a diversified portfolio — VM0044 methodology.

What Biochar Is (And Why It Matters for Your Net-Zero Plan)

A simple definition of biochar for corporate buyers

Biochar is a stable, carbon-rich solid produced by heating organic waste in low-oxygen conditions (pyrolysis), capable of storing atmospheric carbon for centuries to millennia. Unlike fuel-grade charcoal, biochar is purpose-built for carbon removal—converting agricultural residues, forestry waste, and other plant materials into a durable carbon sink. IPCC's Climate Change and Land report notes that biochar can contribute to soil carbon sequestration and climate mitigation when produced and managed with appropriate governance.

For corporate buyers, biochar is a purpose-built carbon removal technology—not a soil amendment that happens to sequester carbon. The carbon locked in biochar comes directly from the atmosphere via photosynthesis and remains stable when applied to soil or embedded in long-lived products.

Key characteristics for procurement:

- Measurable removal: Auditable CO2 drawdown with third-party verification

- Multi-benefit: Improves soil health while addressing waste streams

- Durable storage: Carbon stored in a form that resists decomposition back into greenhouse gases

This distinction matters because your board, auditors, and investors will ask: "Is this really removing carbon, or just delaying its release?" Both the IPCC and the European Commission's Joint Research Centre (JRC) have recognised biochar as a viable carbon removal method with significant potential for carbon sequestration and soil health improvement. These endorsements from authoritative scientific bodies give you the backing needed to defend procurement decisions internally and externally. EU's Joint Research Centre highlights biochar as a soil amendment with potential for carbon sequestration and soil health benefits in its reviews on biochar application to soils.

Why biochar dominates durable carbon removal today

Biochar already delivers over 90% of tracked durable carbon dioxide removal (CDR) and represents more than 3 million tonnes of contracted volume between Q1 2022 and H1 2025. In early 2025, biochar accounted for "over 90%" of durable CDR deliveries, with roughly 0.68 million tonnes delivered and 0.33 million tonnes retired by the end of Q2 2025. This isn't a pilot project or a speculative technology. Biochar is the workhorse of today's carbon removal market.

To put this in context, while direct air capture (DAC) and enhanced weathering capture headlines, biochar is quietly delivering real tonnes at scale. Major corporations, including Microsoft, Google, Swiss Re, and BCG, are already buying biochar carbon removal credits, with individual offtakes including Microsoft's 1.24 million tonne, 10-year agreement with Exomad Green and Google's 100,000 tonne contract with Varaha through 2030. When the world's most data-driven, risk-averse companies are committing multi-year, multi-million-tonne offtakes, that's a strong signal that the technology, verification infrastructure, and commercial viability are mature enough for enterprise procurement.

For DACH corporates building net-zero roadmaps, this concentration of sophisticated buyers offers both validation and a warning. The validation: biochar has been stress-tested by organisations with deep climate science teams and stringent procurement standards. The warning: high demand from Big Tech and financial services is tightening supply and driving prices up, making early engagement with biochar suppliers strategically important.

Biochar should be a dedicated component of your net-zero plan, not a side note. Under frameworks like the Science Based Targets initiative (SBTi) and the Oxford Principles, carbon removals are reserved for residual emissions after aggressive abatement. Biochar fits within a diversified removal portfolio, delivering permanence of hundreds to thousands of years at a cost range of roughly $100–250 per tonne in 2025, positioned between nature-based solutions (<100-year permanence, $25–50/t) and higher-cost engineered options like direct air capture. This makes biochar a rational choice for hard-to-abate sectors looking for durability and auditability without the premium pricing of DAC.

How Biochar Is Made (And What the Process Tells You About Quality)

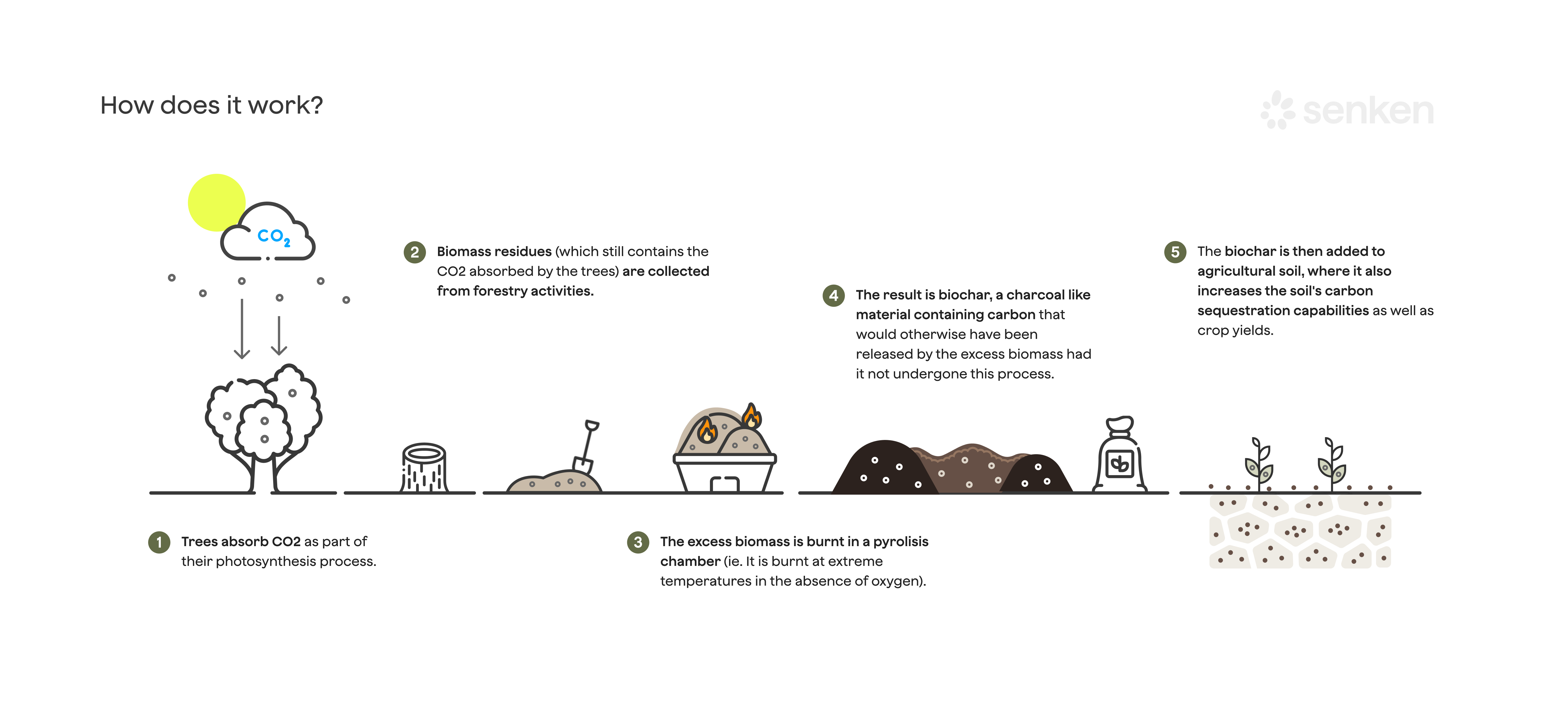

Pyrolysis: the primary biochar process

Pyrolysis is the dominant method for producing biochar and the one you'll encounter most often in high-quality carbon credit projects. The process involves heating biomass to temperatures typically between 350°C and 700°C in an oxygen-starved environment. This controlled heating breaks down complex organic molecules into three outputs: solid biochar (the carbon-rich material you're buying), volatile gases (which can be captured and used for energy), and bio-oils.

What this means for quality: Higher pyrolysis temperatures generally produce more stable, aromatic carbon structures with lower hydrogen-to-organic carbon (H/Corg) ratios. Lower H/Corg ratios signal more condensed carbon bonds that resist microbial decomposition, translating to longer permanence. Projects operating at 500°C+ with well-controlled atmospheres tend to produce biochar with greater stability, but at the cost of lower yield (you get less biochar per tonne of feedstock). When evaluating projects, ask about process temperature, residence time, and oxygen levels. Projects that can't or won't provide this data should raise immediate red flags.

Modern pyrolysis systems also allow for energy recovery. The gases and oils generated during heating can be captured and combusted to power the pyrolysis reactor itself, reducing the project's net energy footprint and strengthening its life-cycle emissions profile. For CSRD reporting purposes, this energy integration becomes a defendable co-benefit and improves the overall carbon accounting.

Gasification: biochar as a co-product of energy

Gasification operates at even higher temperatures (typically 700°C to 1,400°C) with controlled amounts of oxygen or steam, primarily to produce syngas (a mixture of hydrogen, carbon monoxide, and methane) for energy generation. Biochar emerges as a secondary output, representing a smaller fraction of the original biomass compared to pyrolysis.

What this means for quality: Because gasification prioritises energy output, the biochar produced can vary significantly in quality and quantity. The key buyer question: how does the project allocate carbon accounting between the energy product and the biochar? If the project claims full carbon removal credits for the biochar but also sells the energy as "renewable," you need to see a clear methodology that splits emissions reductions (from replacing fossil energy) from removals (from biochar storage). Without transparent allocation, you risk double-counting or overstating the impact.

Credible methodologies from registries such as Puro.earth, Verra VM0044 methodology, Isometric, and the Climate Action Reserve (CAR) include explicit guidance on co-product allocation and stack emissions monitoring. Insist on projects that follow these standards and can provide third-party verification of both energy output and biochar carbon content.

Hydrothermal carbonisation: when the feedstock is wet

Hydrothermal carbonisation (HTC) is designed for wet biomass like sewage sludge, food waste, or algae that would be too energy-intensive to dry for conventional pyrolysis. The process uses water at moderate temperatures (180°C to 350°C) and high pressure to convert the biomass into "hydrochar."

What this means for quality: Hydrochar typically has different chemical properties than pyrolysis-derived biochar. It often contains more oxygen and less aromatic carbon, which can affect stability. Not all hydrochar meets the same permanence thresholds as dry-pyrolysis biochar, so don't assume equivalence. When reviewing HTC projects, demand lab testing of H/Corg ratios, soil stability studies, and independent assessments of long-term carbon retention. ICVCM's 2025 approvals of biochar methodologies explicitly tightened additionality and permanence requirements, making the production process a key audit point. If an HTC project can't demonstrate compliance with these tighter standards, it's not worth the compliance risk.

How Biochar Removes Carbon From the Atmosphere and How Long It Lasts

From photosynthesis to permanent storage: the carbon cycle logic

The biochar carbon removal cycle is straightforward: plants capture CO2 through photosynthesis, converting it into biomass that normally returns to the atmosphere when it decomposes or burns. Biochar short-circuits this return by converting biomass into a stable, carbon-rich solid that resists decomposition.

The step-by-step logic for your board:

- Atmospheric capture: Plants pull CO2 out of the air and lock it in their tissues as they grow.

- Conversion: Biomass is heated under controlled conditions (pyrolysis), transforming carbon into chemically stable aromatic structures.

- Storage: Biochar is applied to soil or integrated into long-lived products, where it can remain stable for hundreds to thousands of years.

- Net removal: Because the carbon originated in the atmosphere and is now stored in a form that won't readily re-release, you've achieved net CO2 removal.

This is fundamentally different from avoided emissions—biochar is pulling existing CO2 out of the air, which is why it commands a higher price and stronger climate confidence.

Permanence metrics: H/Corg ratios, lab tests and standards

Permanence is the defining quality metric for biochar carbon credits, measured primarily by the hydrogen-to-organic carbon (H/Corg) molar ratio. Lower ratios indicate more aromatic, stable carbon structures that resist decomposition. Most credible methodologies set H/Corg thresholds to ensure long-term storage:

- Puro.earth typically requires H/Corg <0.7 for soil-applied biochar.

- Verra VM0044 v1.2 and Isometric's Biochar protocol similarly define permanence periods based on H/Corg and other stability tests.

- ICVCM's 2025 approval of these methodologies confirms that projects meeting these thresholds are eligible for high-integrity labels and compliance-ready credits.

These permanence criteria are reflected in widely adopted standards, such as Verra VM0044 v1.2 and ICVCM CCP labeling.

What this means in practice: When evaluating a biochar project, request third-party lab certificates showing H/Corg ratios and compliance with the chosen methodology's permanence criteria. Projects that cannot provide this data or rely on outdated methodologies should be rejected. For CSRD and audit purposes, lab-verified permanence is the evidence you need to defend the "durability" claim in your sustainability reports.

Senken's Sustainability Integrity Index (SII) assesses permanence and reversal risk using over 350 data points per project within its Carbon Impact module, giving you a quantitative, comparable score across biochar suppliers. This layered approach (methodology compliance + lab data + independent ratings) is what transforms biochar from a "trust us" claim into an auditable fact.

What Biochar Does for Soil and Circularity (Co-Benefits You Can Defend)

Soil health: nutrient retention, water and microbial life

Biochar's agronomic benefits are well-documented and provide defensible co-benefits for your sustainability narrative:

- Nutrient retention: The porous structure increases soil's cation exchange capacity (CEC), holding nutrients like nitrogen, phosphorus, and potassium that would otherwise leach away—reducing fertilizer runoff into waterways.

- Water-holding capacity: The internal pore structure acts like a sponge, retaining moisture during dry periods and reducing irrigation needs in sandy or degraded soils.

- Microbial habitat: Biochar creates habitat for soil microbes and mycorrhizal fungi that play critical roles in nutrient cycling, disease suppression, and soil structure formation.

What you can claim: Improved CEC, water retention, and microbial activity are scientifically supported. What you should not claim without project-specific data: Dramatic yield increases or guaranteed drought resilience—yield improvements are context-dependent and often modest (5-15% in well-designed trials). Use conservative language like "enhanced nutrient and water efficiency" that will survive regulatory scrutiny.

Circular economy: turning waste streams into assets

Biochar production turns agricultural and forestry residues that would otherwise be burned, landfilled, or left to decompose into valuable carbon sinks and soil amendments. This directly addresses waste management challenges, particularly in rural and peri-urban areas where waste disposal infrastructure is limited.

For DACH corporates with biomass-intensive operations or supply chains (food processing, forestry, agriculture, landscaping), biochar offers a pathway to valorise organic waste internally. Instead of paying for disposal or composting, biomass can be converted on-site or through local partnerships into biochar, generating carbon removal credits and creating a usable soil product for farms, parks, or landscaping.

Co-benefit for CSRD: Circular economy contributions are a core pillar of ESRS E5 (Resource Use and Circular Economy) reporting under CSRD. Documenting how biochar projects close waste loops, reduce landfill methane, and create value from residues directly supports your circular economy disclosures. Quantify the waste tonnage diverted, the methane emissions avoided, and the downstream agronomic or product benefits to build a robust, evidence-based co-benefit narrative. ESRS E5 – Resource Use and Circular Economy (draft PDF)

Which co-benefits can you credibly claim under CSRD

Under CSRD's European Sustainability Reporting Standards (ESRS), companies must disclose impacts, risks, and opportunities across environmental, social, and governance dimensions. Biochar's co-benefits can support multiple ESRS topics, but only if documented:

- ESRS E1 (Climate Change): Primary impact is durable CO2 removal. Document permanence, methodology, and verification.

- ESRS E2 (Pollution): Reduced particulate and methane emissions from alternative waste disposal (if applicable); improved air quality from reduced open burning.

- ESRS E3 (Water and Marine Resources): Reduced nutrient leaching and improved water-use efficiency in agriculture (requires field-level monitoring).

- ESRS E4 (Biodiversity and Ecosystems): Soil health improvements and habitat creation for soil organisms (requires biodiversity assessments).

- ESRS E5 (Resource Use and Circular Economy): Waste valorisation, closed-loop biomass cycles, reduced reliance on virgin fertilisers.

- ESRS S1 (Own Workforce) and S2 (Workers in Value Chain): Job creation, farmer livelihoods, and capacity building (requires social impact data from projects).

Senken's SII 'Beyond Carbon' module assesses impacts on soil, water, biodiversity, and livelihoods using 105 data points, providing quantified co-benefits that directly map to CSRD's multi-dimensional impact requirements. Use project scorecards, third-party audits, and field monitoring data to back up your co-benefit claims, and avoid generic statements without evidence.

Standards, registries and integrity updates (2024–2025)

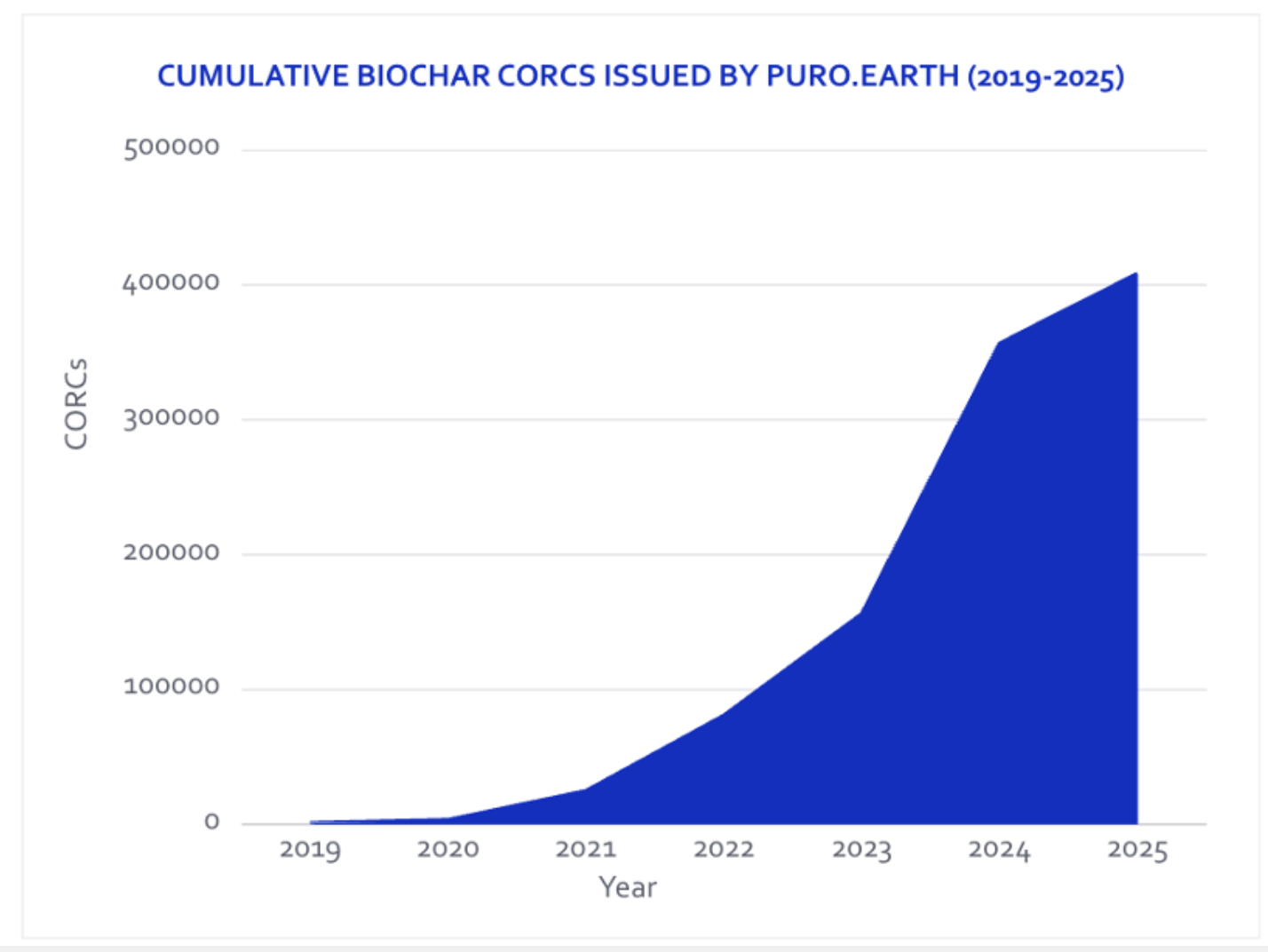

- Puro.earth milestone: 1 million CORCs issued since 2019 by March 2025; biochar and geologically stored carbon were the two largest methodologies by issuance. Puro.earth's October 2025 biochar report highlights >400,000 biochar CORCs issued by mid-2025 and strong buyer uptake.

- Verra (VM0044): Minor revision to v1.2 (June 27, 2025) adds investment analysis for additionality and aligns with ICVCM. VM0044 is active; Verra registered the first biochar project in October 2024.

- ICVCM approvals: In 2025, ICVCM approved Verra VM0044 (v1.2), Isometric's Biochar Production & Storage, and CAR's U.S./Canada Biochar methodologies. ICVCM notes 25 Isometric biochar projects are registered with ~500,000 credits expected in 2026, and three VM0044 projects with ~249,000 annual credits.

Downsides and Challenges of Biochar You Need to Manage

Feedstock competition and land-use concerns

Not all biomass used for biochar is truly "waste." If a project sources roundwood, timber-grade logs, or biomass that could be used in long-lived wood products (furniture, construction), you're effectively shifting carbon from one pool to another rather than achieving net removal. Similarly, if biochar production incentivises land clearing, monoculture expansion, or unsustainable harvest, the net climate benefit can be zero or negative.

How to mitigate: Require detailed feedstock sourcing documentation. Ask for:

- Waste classification: Legal status of the feedstock as residue or by-product.

- Sustainability certificates: FSC, PEFC, or equivalent for forestry biomass; Rainforest Alliance, Fairtrade, or organic for agricultural residues.

- Additionality evidence: Proof that the biomass was not already allocated to higher-value uses or carbon sequestration pathways.

- Land-use assessments: Satellite imagery or third-party audits confirming no land-use change or deforestation associated with feedstock production.

Projects that refuse to provide this documentation or operate in high-deforestation regions without transparent monitoring should be avoided, regardless of their headline removal claims.

Technology, emissions and local air quality

Poorly designed kilns or uncontrolled combustion can produce significant particulate matter (PM2.5, PM10), methane, and other pollutants that undermine the net climate benefit and create local air quality problems. In regions with strict EU or German air quality standards, this is a direct compliance risk.

How to mitigate: Insist on projects with modern, engineered pyrolysis or gasification systems that include emission control technologies (scrubbers, filters, gas capture). Request full life-cycle assessments (LCAs) that quantify process emissions, energy inputs, and net carbon removal. Projects should provide third-party-verified emissions data and demonstrate compliance with local air quality regulations. Methodologies approved by ICVCM (Verra VM0044, Isometric, CAR, Puro.earth) include requirements for emission monitoring and net removal calculations that account for process emissions. If a project can't show you an LCA or emissions monitoring plan, it's not investment-grade.

Market constraints, buyer competition and supply risk

Big Tech-led demand for biochar is creating a supply crunch. Reuters reported tightening supply driven by large offtakes from Microsoft, Google, Swiss Re, and other major buyers. With 3.04 million tonnes contracted between Q1 2022 and H1 2025, but only 0.68 million tonnes delivered by the end of Q2 2025, there's a significant gap between forward commitments and actual issuance.

Notably, Verra VM0044 is one of the ICVCM-approved methodologies shaping this market. Verra VM0044 is the specific standard used for many biochar projects, and ICVCM-approved methodologies help ensure credits meet high integrity criteria.

What this means for mid-sized DACH corporates: If you wait until 2026 or 2027 to start procurement, you may find that the highest-quality, best-documented biochar projects are already fully contracted to multi-year offtakes. Prices will also likely continue rising as demand grows and regulatory mandates (like SBTi's expected removal requirements) take effect.

How to mitigate: Start procurement conversations early. Consider multi-year forward purchase agreements to lock in price and supply. Work with partners like Senken, who maintain relationships with verified suppliers and can aggregate demand across clients to secure better pricing and access. Diversify your removal portfolio across multiple projects, geographies, and methodologies to reduce dependence on any single supplier or technology.

How to Evaluate Biochar Carbon Credits: A Due-Diligence Checklist for Companies

Documentation and traceability you should always request

Build a standardised request-for-information (RFI) template for all biochar suppliers:

- Project design document (PDD) or equivalent, including methodology, baseline scenario, and monitoring plan.

- Feedstock sourcing agreements or contracts, with waste classification and origin documentation

- Production technology specifications: Reactor type, operating temperature, residence time, and emission controls.

- Lab certificates: H/Corg ratios, carbon content, heavy metal testing (if soil-applied), and stability assessments.

- MRV (Monitoring, Reporting, Verification) plans with a third-party verification schedule and auditor details.

- Registry IDs and issuance records: Link to public registry pages showing issued, delivered, and retired credits.

- Chain of custody: Traceability from feedstock collection → production → biochar application, with GPS coordinates and photographic or satellite evidence.

- Delivery and retirement schedules: Timeline for credit issuance, forward commitments, and retirement windows.

Senken provides ready-to-use evidence packs that compile this documentation into a single CSRD-ready submission, reducing your team's workload while maintaining full traceability.

Additionally, financials and dependence on carbon revenue

Additionality is the cornerstone of credible carbon credits: the project should not have happened without carbon finance. For biochar projects, this often hinges on financial viability. Ask:

- What share of project revenue comes from carbon credit sales? If it's 60%+, the project is likely additional (biochar production wouldn't be economical without carbon revenue). If it's <20%, scrutinize whether the project would have happened anyway.

- Investment analysis: Request the project's investment decision documentation or financial model showing that carbon revenue was critical to securing financing or making the business case.

- Verra VM0044 v1.2 added investment analysis requirements for additionality, and ICVCM approvals reinforce these expectations. Projects following updated methodologies should have this documentation on hand.

- Alternative funding sources: If the project also generates renewable energy, compost, or other co-products, how is revenue allocated? Ensure carbon credits are only issued for the biochar-sequestered carbon, not double-counted with energy or compost benefits.

If a project cannot demonstrate financial additionality or provide transparent investment analysis, it's not a defensible purchase for compliance-grade portfolios.

Legal, CSRD and greenwashing red flags

Avoid projects that exhibit the following warning signs:

- Vague feedstock claims: "Agricultural waste" without specifying type, origin, or documentation.

- No life-cycle assessment: If they can't show net removal calculations, assume the worst.

- Opaque registry entries: Missing issuance records or credits issued under outdated methodologies.

- Poor external ratings: BeZero C/D ratings, Sylvera low scores, or flagged risks from rating agencies.

- Controversial locations: Projects in regions with active deforestation, land conflicts, or regulatory violations.

- Exaggerated co-benefit claims: Promises of "carbon neutrality" or "regenerative agriculture" without field-level monitoring data.

German greenwashing litigation, the EU Green Claims Directive, and CSRD's ESRS E1 climate requirements all demand transparency and evidence-backed claims. Any credit or project that can't meet these standards exposes your company to reputational and legal risk.

Checklist summary:

Biochar Market Pricing, Volumes and the Current Buyer Landscape

Biochar carbon credit prices today and why they're higher than avoidance

Nasdaq/Puro.earth's CORC Biochar Price Index (CORCCHAR) shows prices of approximately €125–€145 per tonne in 2025, with a published value of €125.42 in October 2025. (puro.earth)

Why the premium? Biochar delivers durable, engineered removal with centuries-to-millennia permanence, transparent third-party verification, and low reversal risk. It's not avoiding future emissions or relying on uncertain biological systems; it's physically pulling CO2 out of the air and locking it in a stable form. For companies targeting SBTi net-zero commitments or preparing for future regulatory requirements that distinguish high-durability removals from short-term or avoidance credits, this premium is the cost of climate confidence.

How to explain this to your CFO: Frame biochar as the "compliance-grade, audit-ready" option in your carbon removal portfolio. While the per-tonne price is 3-5x higher than avoidance credits, the reputational risk and reversal risk are a fraction of lower-quality alternatives. If your internal carbon price is €50–€100/t, biochar at €125–€145/t represents a 25-50% premium for permanence and defensibility—rational insurance against greenwashing accusations and future regulatory tightening.

Market volumes, deliveries and delivery risk

Publicly disclosed biochar carbon removal contracts totalled 3.04 million tonnes between Q1 2022 and H1 2025, with 1.6 million tonnes contracted in H1 2025 alone. However, only about 0.68 million tonnes had been delivered and 0.33 million tonnes retired by the end of Q2 2025.

What this means: There's a large gap between forward commitments and actual credit issuance. Many buyers, including Big Tech, have signed multi-year offtakes (buying future credits at negotiated prices), but projects are still ramping up production, completing verification cycles, and issuing credits in batches. This delivery lag is normal for emerging CDR markets, but it introduces timing risk: if you need credits for immediate retirement in your 2025 sustainability report, forward-only deals won't help.

How to manage delivery risk:

- Mix spot and forward purchases: Buy some credits that are already issued and available for immediate retirement (spot) to cover near-term reporting needs, and lock in forward contracts for future years to secure price and supply.

- Diversify across suppliers and vintages: Don't commit your entire removal volume to a single project or developer. Spread risk across multiple verified projects with proven issuance histories.

- Use public registries to verify delivery track records: Puro.earth Registry, Verra, Isometric, and CAR provide transparent issuance and retirement ledgers. Check how many credits a project has issued historically, how quickly they retire, and whether the developer has a backlog or delivery issues.

Who is buying biochar (and what that means for DACH corporates)

Microsoft, Google, BCG, Swiss Re, and JPMorgan are among the top biochar carbon removal purchasers by volume through H1 2025. Individual offtakes include Microsoft's 1.24 million tonne, 10-year agreement with Exomad Green, Google's 100,000 tonne contract with Varaha, Swiss Re's 70,000 tonne agreement via Carbonfuture, and BCG's 50,250 tonne durable CDR purchase including biochar from Exomad and Euthenia Energy.

Implications for DACH corporates:

- Supply tightness: These large, multi-year commitments are locking up significant portions of high-quality biochar supply. If you wait until 2026–2027, you may face limited availability and higher prices.

- Quality signal: The concentration of sophisticated, risk-averse buyers (Microsoft, Google, Swiss Re) is a strong integrity signal. These organisations conduct deep technical and financial due diligence; if they're comfortable with biochar, it's a mature, credible pathway.

- Price expectations: Large buyers often negotiate volume discounts and forward pricing that may not be available to smaller purchasers. Mid-sized and large DACH corporates should consider aggregating demand through platforms or partnerships (such as Senken) to access better pricing and supply.

- Competitive positioning: Early movers in biochar procurement are positioning themselves as climate leaders and securing stable, long-term removal strategies. Late movers risk being seen as reactive or dependent on lower-quality, higher-risk credits when supply runs short.

Notable Biochar Suppliers and Geographies for Portfolio Diversification

Europe and DACH-relevant biochar suppliers

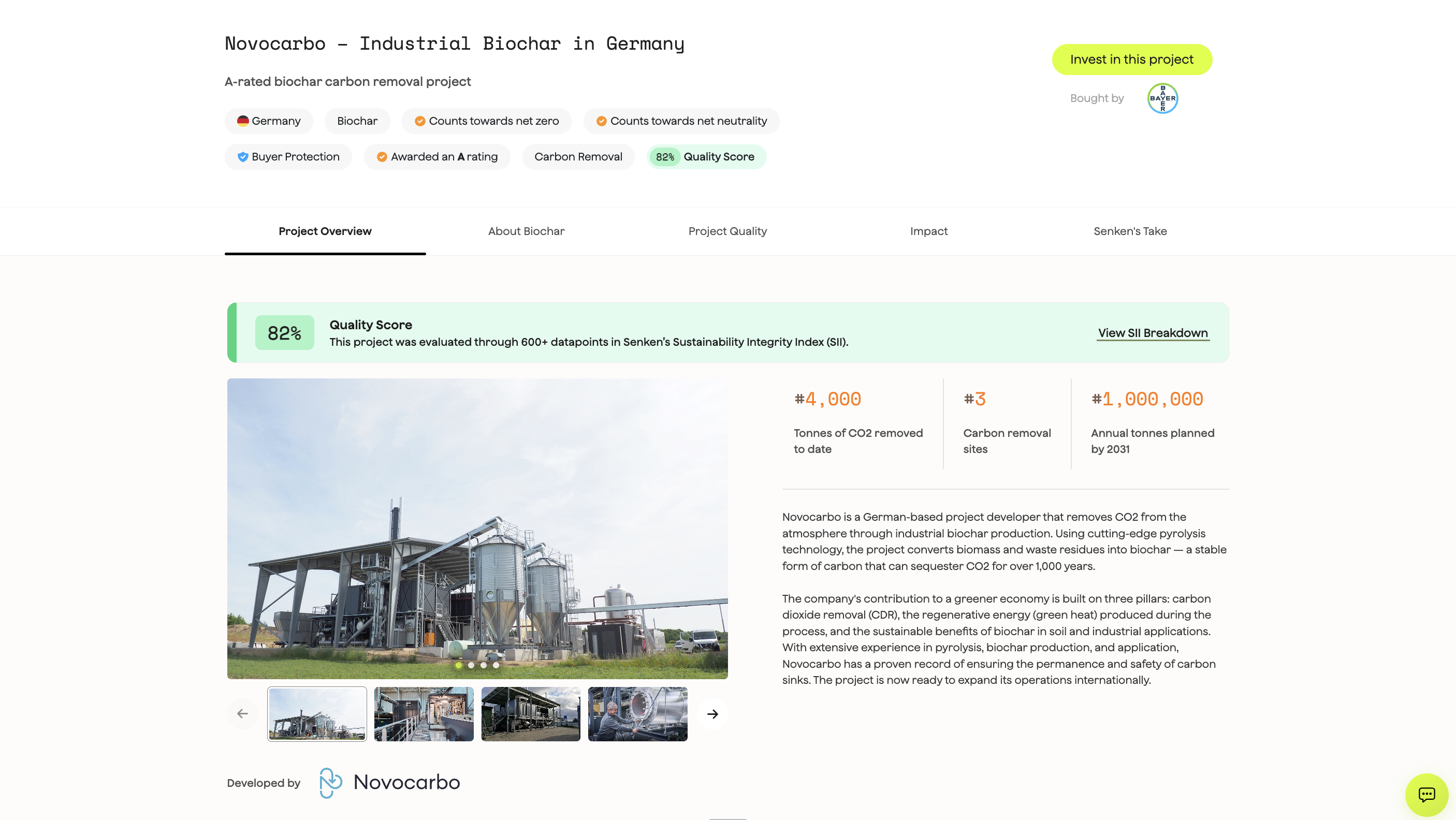

Novocarbo (Germany) is a leading industrial biochar producer using cutting-edge pyrolysis technology to convert biomass and waste residues into biochar with over 1,000 years of carbon storage. The project is certified by Puro.earth and offers high permanence (>10,000 years), local DACH implementation, and innovative biochar applications in industrial and agricultural settings.

Why these matter for DACH buyers: Local or regional European projects offer shorter supply chains, easier site visits and audits, and alignment with EU regulatory frameworks (CSRD, Green Claims Directive). They also reduce geopolitical risk and currency exposure compared to projects in emerging markets.

Americas: industrial-scale producers

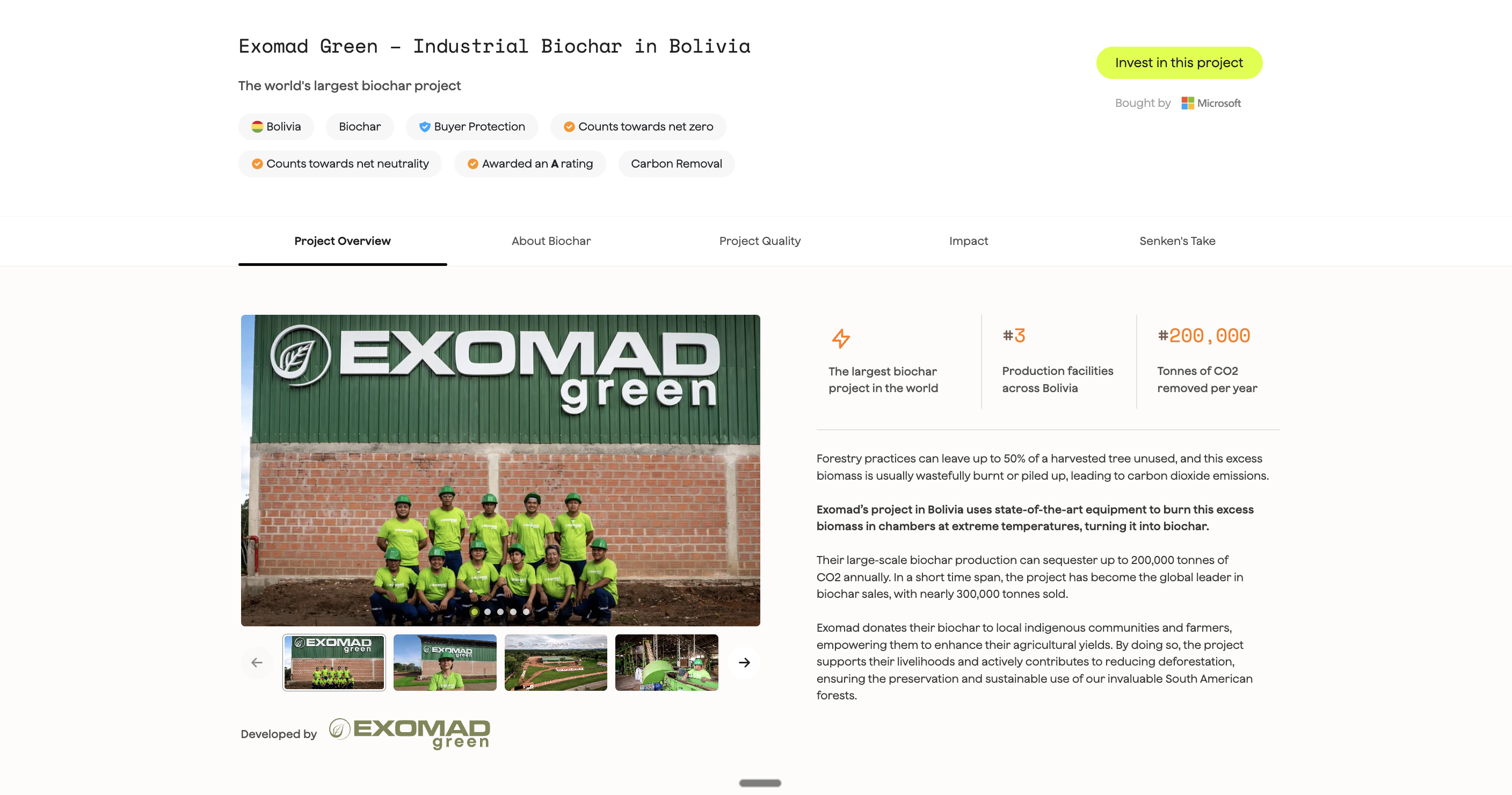

Exomad Green (Bolivia) operates the world's largest biochar project, producing up to 200,000 tonnes of CO2 removal annually by converting excess forestry biomass into biochar. The project has issued nearly 300,000 tonnes of credits and secured Microsoft's 1.24 million tonne, 10-year offtake, demonstrating industrial scale and buyer confidence.

Why these matter: The Americas, particularly the United States and Latin America, offer large-scale, industrialised biochar production with mature verification infrastructure. These projects demonstrate that biochar can operate at the scale required to meet corporate multi-year commitments, and they provide geographic diversification outside Europe.

Africa and Asia: emerging supply and co-benefits

Varaha (India) runs both artisanal and industrial biochar projects. The artisanal project addresses invasive Prosopis juliflora, restoring native grasslands and supporting local livelihoods, while the industrial project (India's first Puro.earth-certified industrial biochar) uses pyro-gasification to convert corn waste into high-carbon biochar distributed to local farmers. Google signed a 100,000 tonne offtake with Varaha.

Why these matter: Africa and Asia offer high-impact, smallholder-linked projects with strong co-benefits (livelihoods, soil restoration, food security). For companies with sustainability narratives focused on social impact, climate justice, or supporting communities on the frontlines of climate change, these projects provide compelling stories backed by credible verification. They also introduce geographic diversification and can strengthen your ESG positioning under CSRD's social reporting standards (ESRS S2, S3).

Regional diversification strategy:

- Europe (30-40%): Prioritise for regulatory alignment, proximity, and ease of due diligence.

- Americas (30-40%): Leverage industrial scale, proven track records, and mature verification infrastructure.

- Africa and Asia (20-30%): Include for high co-benefits, social impact, and geographic diversity.

How Biochar Fits Into Your Carbon Removal and CSRD Strategy

Positioning biochar among other removal methods

Use a simple permanence-and-cost matrix to explain biochar's role internally:

Biochar sits in the "novel but mature" durable removal bucket, offering century-scale storage at materially lower cost than DAC, making it a strong candidate for residual emissions in a diversified portfolio.

Strategic guidance: Start with a portfolio that includes both nature-based removals (for cost-efficiency and co-benefits) and durable, tech-based removals (for permanence and compliance readiness). Align with draft Net-Zero Standard Version 2, which introduces ongoing emissions responsibility and a staged pathway toward durable removals. Biochar allows you to begin meeting that expectation today without paying DAC prices.

Designing a diversified portfolio and phasing procurement

Phase 1 (2025–2027): Allocate 20–30% of your carbon removal budget to biochar, focusing on high-quality, ICVCM-eligible projects with proven issuance histories. Lock in multi-year forward contracts to secure price and supply before regulatory mandates drive further demand.

Phase 2 (2028–2035): Increase the biochar allocation to 40–50% of your durable removal portfolio as supply scales, methodologies mature, and your internal carbon accounting systems integrate removals into routine reporting. Add enhanced weathering or DAC as the budget allows.

Phase 3 (2035–2050): Target a balanced portfolio of 50% durable tech-based removals (biochar, enhanced weathering, DAC) and 50% high-quality nature-based removals, aligned with SBTi's expected permanence requirements and your residual emissions profile.

Procurement tactics:

- Spot purchases for immediate retirement needs and annual reporting.

- Multi-year forward offtakes (3–5 years) to lock in price, secure supply, and align with your decarbonisation roadmap.

- Aggregated procurement through platforms like Senken to access better pricing, share due diligence costs, and pool volume across multiple buyers.

Senken provides evidence packs, Sustainability Integrity Index scorecards, and CSRD-ready documentation that allow you to operationalise this policy without building an in-house biochar lab or carbon science team. This positions you as a compliance leader, not a laggard scrambling to catch up when auditors start asking hard questions about your 2025–2027 carbon credit purchases.

Frequently Asked Questions

What is the controversy with biochar?

The main controversies centre on feedstock sourcing (using virgin timber instead of waste), production emissions from poorly designed systems, and quality variability in permanence. Mitigate these risks by demanding transparent feedstock documentation, third-party-verified life-cycle assessments, and lab-tested H/Corg ratios below 0.7 from ICVCM-approved projects.

How much do biochar carbon credits cost?

Biochar credits typically range from €125–€145 per tonne in 2025 based on the Nasdaq/Puro.earth CORCCHAR index—3-5× higher than avoidance credits, reflecting century-to-millennia permanence and low reversal risk. Frame this to your CFO as compliance-grade insurance against greenwashing accusations and future regulatory tightening.

Can biochar be used with compost?

Yes—combining biochar with compost pre-loads the porous structure with nutrients and beneficial microbes, delivering immediate fertility benefits alongside long-term carbon storage. Ensure the project's carbon accounting clearly separates biochar removal credits from composting benefits to avoid double-counting.

Where is biochar produced in the USA?

Major Puro.earth-certified U.S. producers include Oregon Biochar Solutions (Oregon), Standard Biocarbon's ReGenerate Livermore Falls (Maine), and Wakefield Biochar operating across multiple locations. Production concentrates in regions with abundant forestry residues (Pacific Northwest, Northeast) and agricultural residues (Midwest, South).

Which companies are buying biochar carbon credits?

Major buyers include Microsoft (1.24 million tonnes over 10 years), Google (100,000 tonnes through 2030), Swiss Re (70,000 tonnes), and BCG (50,250 tonnes in 2024). This concentration of sophisticated, risk-averse buyers signals that biochar has been stress-tested for quality and auditability—and that high-quality supply is tightening.

How do I integrate biochar credits into CSRD reporting?

Biochar credits support ESRS E1 (Climate Change) for durable removal, ESRS E5 (Circular Economy) for waste valorisation, and ESRS E4/E3 for documented co-benefits. Demand CSRD-ready evidence packs from suppliers: registry IDs, H/Corg lab certificates, feedstock sourcing documentation, life-cycle assessments, and independent ratings like Senken's Sustainability Integrity Index.

What's the difference between biochar carbon credits from different registries?

The core difference lies in methodology rigour and ICVCM alignment—prioritise credits issued under ICVCM-approved methodologies (Puro.earth, Verra VM0044 v1.2, Isometric, CAR) and verify each project's registry records and independent ratings, as project-level quality still varies within each registry.